Let the Games Begin: Halftime - Part II

11.22.2017

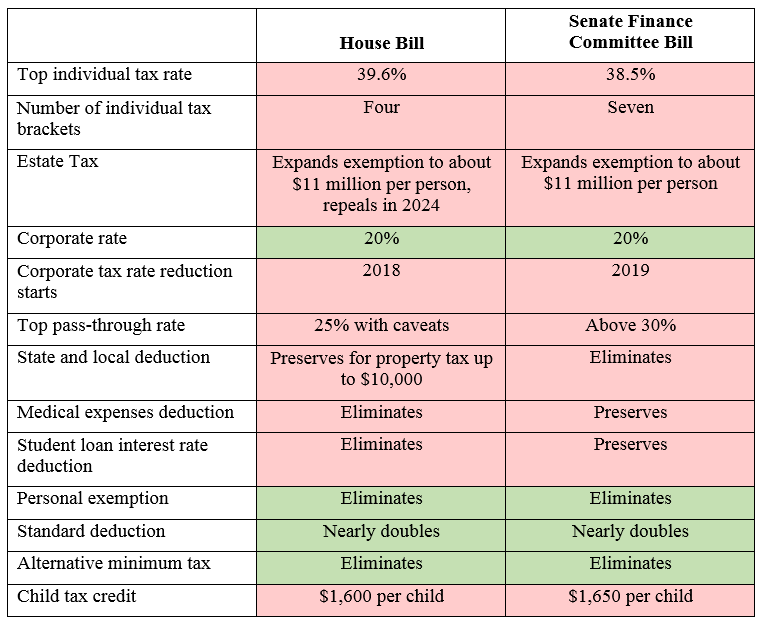

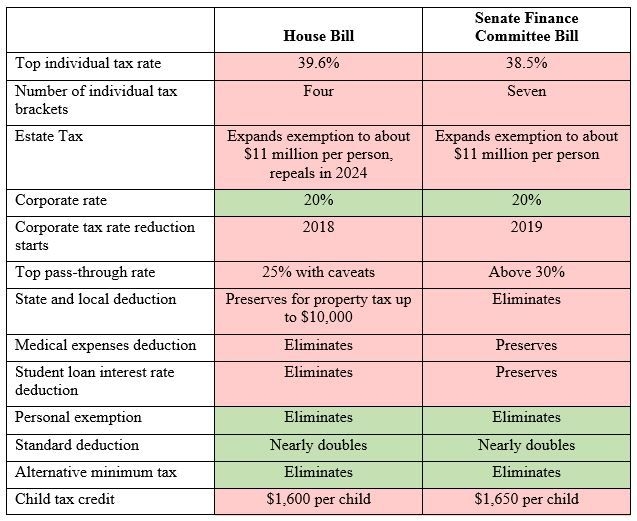

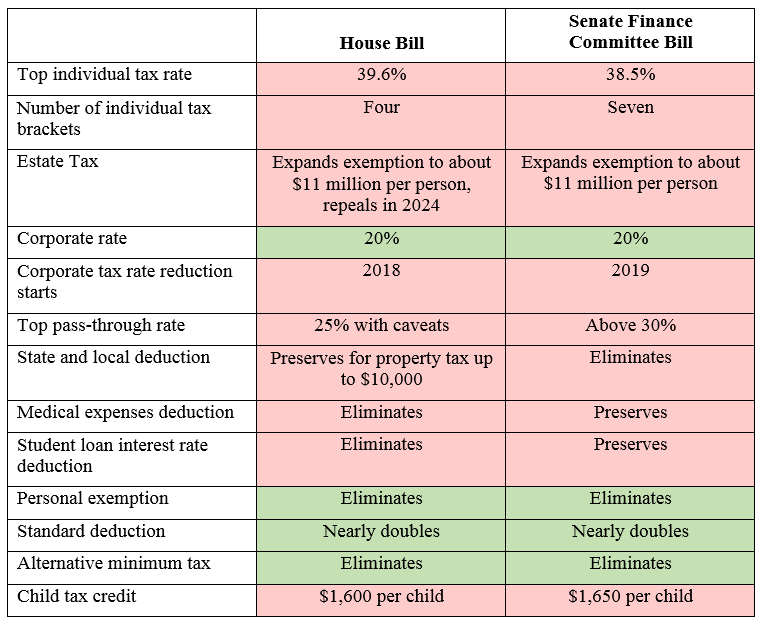

Earlier this fall I detailed in a client advisory, President Trump’s proposals for changing the tax code. Since that time the Republican majority in the House of Representatives has passed a tax bill (“H.R.1”). The Senate Finance Committee has marked up its own Bill for consideration. It is expected that the Senate Finance version will be taken up by the Senate after Thanksgiving. Here is a comparison of the major differences between the House legislation and the Senate Finance Committee version as of Thanksgiving week. This list of differences highlight the domestic law provisions and does not address the international tax provisions.

Already, there are serious questions as to whether the Senate Finance Committee Bill can clear the Senate in its present form. I believe that a number of changes will need to be made before it can pass the Senate. That is because the Republicans have only a two vote majority in the Senate and in order to pass the law without the votes of any Democrats, 50 Republicans will need to agree on the Bill.

Several Republican senators have already asked for changes in the Senate Finance Committee Bill as a condition for their vote. They have raised four major issues as follows:

- The Senate Finance Committee version repeals the mandate under the Affordable Care Act that requires everyone to obtain health insurance. Some senators have voiced concern that removing this mandate will gut the Affordable Care Act and might raise health care premiums for many, as the insurance pool will shrink without the participation of a large number of participants.

- Republican senators from states with high taxes, have expressed concern that the Senate Finance Committee Bill provides no deduction for state and local taxes. The House provision contains a deduction for state and local real estate property taxes subject to a $10,000 cap. The Senate Finance version had no deduction at all for state and local tax.

- One senator has raised a question regarding unfair treatment of small businesses compared to corporations. Corporations are afforded a 20% maximum tax rate. Small businesses, not in corporate form, can be taxed at a higher rate.

- Finally, some Senate Republicans have voiced concerns about the impact of this legislation on the federal deficit. The federal deficit is expected to increase by $1.5 trillion dollars over the next ten years under their proposal. Increasing the deficit can cause interest rates to rise, which in turn can increase the value of the dollar, which in turn can disadvantage U.S. companies which export their products abroad. In short, deficit financed tax cuts can end up hurting the economic expansion the tax cuts were designed to encourage.

Tax Planning Suggestions

At this point there is at least a strong likelihood that a tax Bill will pass the Congress effective in 2017. Under both versions of the legislation, itemized deductions are likely to be significantly reduced. If you can benefit from itemizing deductions now, be sure to make the expenditures this year to fully utilize them this year. Prepay your state and local tax estimates due in January 2018. See your doctor and dentist and pay for prescriptions this year. Be sure to pay for medical insurance premiums this year. Prepay your January home mortgage payment in December. Make your charitable contributions this year. If you have an ongoing pledge commitment for the coming year, prepay it now. Consider using highly appreciated stock to fund your gift, instead of cash. Make sure that bills for tax preparation, investment management fees, and employee business expenses are paid this year.

Whether or not you itemize deductions, review your stock portfolio and consider realizing losses in your portfolio to offset gains. If you can still make contributions to a tax deferred retirement or savings plan, make an added contribution this year.

If you have tax planning questions, we are here to assist you. Please call us if you need assistance. We will be preparing another client advisory if and when a final tax Bill passes the Congress.

If you have questions about the potential tax reform and how it may affect your business, please contact Kenneth Ahl at (215) 246-3132 or kahl@archerlaw.com or any member of Archer's Tax Group in Haddonfield, N.J., at (856) 795-2121, in Princeton, N.J., at (609) 580-3700, in Hackensack, N.J., at (201) 342-6000, in Philadelphia, Pa., at (215) 963-3300, or in Wilmington, Del., at (302) 777-4350.

DISCLAIMER: This client advisory is for general information purposes only. It does not constitute legal or tax advice, and may not be used and relied upon as a substitute for legal or tax advice regarding a specific issue or problem. Advice should be obtained from a qualified attorney or tax practitioner licensed to practice in the jurisdiction where that advice is sought.

Featured Insights

05.16.2024

Speaking Engagements & Seminars

Gianfranco Pietrafesa & Mark Oberstaedt to Speak on LLCs at NJ State Bar Association Annual Meeting

Partner Gianfranco Pietrafesa will be moderating his annual “What’s New with LLCs?” seminar at the New Jersey State Bar Association Annual Meeting. Gianfranco brings his extensive background on New Jersey LLC law to the panel having served on the select committee that drafted the New Jersey Revised Uniform Limited Liability Company Act. Joining him on the panel will be partner Mark Oberstaedt.

05.09.2024

Speaking Engagements & Seminars

Gianfranco Pietrafesa and Shamila Ahmed to Present “A Refresher on the New Jersey Revised Uniform Limited Liability Company Act” to the Hudson-Bergen Inn of Transactional Counsel

Gianfranco A. Pietrafesa and Shamila R. Ahmed, members of the firm's Business Counseling and Merger & Acquisitions Groups, will give a presentation on New Jersey LLC law to members of the Hudson-Bergen Inn of Transactional Counsel. The presentation information is as follows:

04.17.2024

Client Advisories